Beyond Mathematical Odds - Continuous energy crunch

Part I

The last time I wrote one of these, weeks ago, I had fewer subscribers than now, so in case you are new, one side of this Substack is science, mainly focused on SARS-CoV-2 and its complex cascade, into many levels of human health.

The other is tracking, observing, and forecasting the non-linear cascade dynamics involved in the SARS-CoV-2 response, vulgarly known as the 2020 global lockdowns. Logistics, food, grains, farming, supply chain, human behavior, in short, “complexity”. Pieces titled “Beyond Mathematical Odds” are the main parts of a long-running series about these cascade effects. I stopped writing for a while because:

Diminishing returns, little changes, in turn becoming repetitive observations

Waiting for the dynamics to play out, therefore more data to make my points

Some time off, so people don’t get as depressed

Many of the points I am about to make might sound light on data and evidence, but you should refer back to other “BMOs” in that case. The same cascade is still applying.

Energy

When I began writing about the energy sector and attempting to demonstrate how impactful energy is to any system, but rather more important to complex systems, I shortly wrote about nuclear energy, and how countries would find themselves between hard choices, attempting to walk back policies, nuclear as green and finally using nuclear, but lack of investment would have consequences.

One of France’s most modern nuclear power plants closed months ago for maintenance and now, after many months they found a cracked pipe. Taking longer for this plant to come back only, which is a problem, because half of France’s 56 reactors are offline, leading to more disputes in a tight energy market, given that France will import energy.

Such is the situation of what once was an energy-exporting nation, where France finds itself both importing energy now, and its energy regulator has asked residents in homes and businesses to cut their energy use. Besides other effects on the industry, one of most concerns is the impact on drug production, leading the French pharmaceutical industry to issue a press release asking he French government to adopt national-level measures to tackle this “imminent danger”.

The same is happening elsewhere in the EU.

Essential drugs are usually generic and, therefore, low profit, meaning that only the most efficient suppliers can remain competitive. "In Spain for example, and while production costs have risen at least 10% as a result of 150%, 112%, and 93% rises in the cost of gas, electricity, and water, respectively, absorbing this rise in manufacturing costs immediately compromises the country competitiveness of essential medicines production," the Teva report said.

"At the very least, they seem to be cautious about this upcoming winter, with it worsening next winter, since the energy supplies previously purchased could be running very low by then," he said. "Beyond that issue, it's pure speculation; however, it's reasonable to assume that the cost of production will continue to rise with lower revenue generation, especially from generic drugs."

Per what the pharmaceutical industry itself says, and taking into consideration the larger trend in other countries (China, and especially India), one can safely expect that prices for drugs to keep somewhat at the higher end, prone to further supply chocks and very real chances of unexpected severe shortages, per what I wrote recently in my drug shortage substack. Something the reader may take into consideration going further. I also recommend you read this entire piece about the energy crisis and its impact on the textile industry.

Similar to the exact scenario I outlined earlier this year, one in which I wrote governments found themselves between a rock and a hard place and their short-sighted actions would just lead to more pain later on, the German government chose the “easy way out” insuring maximum pain later on, by introducing a price cap in January of 2023. This does nothing to address the underlying issues, which are not capital, but supply-related, pushing Germany and after a while the entire block to what I wrote months ago.

Germany is under severe and real threat of deindustrialization, wiping out swaths of the middle class, dragging the entire economic block down the drain (which is already doing), and losing most of its industry. For the last 4 weeks many German papers were talking about this serious threat, and as of 3 days ago even some of the top brass of the government stated the same.

Thus, 90% of the surveyed entrepreneurs reported that the increased energy and raw materials prices became an existential threat to them.

Every fifth company is already considering the possibility of transferring production abroad

Energy-intensive enterprises of the chemical, steel, and paper industries have reduced or stopped production, and the fertilizer manufacturer SKW Piesteritz has closed.

One of the biggest trends which I forecasted months ago was how an everyday occurrence strikes would become, and for a short while I did cover many of them, but at some point, I opted to start covering each one, because of how common it was becoming. As many wrote back as months went by, inflation and loss of purchasing power would lead to waves of strikes, Germany’s biggest union warn about this exact scenario. France refinery workers have been going on for as long as 50 days, further complicating the energy and fuel situation. Different industries in Italy, Britain, and elsewhere are all threatening to strike, the list increases almost weekly. Iran, Iraq, and neighbors in the region are also going on a severe strike right now.

Why do I bring these examples up ? Repeating myself, which I often do when it comes to forecasting, this isn’t the middle of the road yet, indeed this will only increase in frequency and disruptive impact on both the economy and supply chain. With one of the biggest and most impactful ones is the US rail workers strike, which can impact the entire global supply chain function, and tilt markets and supply in and on itself.

Third U.S. union rejects national rail contract deal

After talking about energy, we must cover the second most important aspect of any functional economy and the byproduct of energy itself. Fuel.

Another outlined dynamic coming into play is the global fuel shortage caused by Europe’s misguided decisions when it comes to gas, green policies, and everything in between. The shift in markets where LNG cargo goes achieves a great impact on poorer countries, and as it did occur this entire year, this will drive unrest in the future, and the only saving grace as they not popping up right now was the drastic changes in weather in said countries (which will impact other dynamics).

The situation is dire enough that such an aggressive shift away from Russian gas impacted the LNG market in such a way that the market will be short of proper supply until at least 2026 (another one of my forecasted timelines criticized earlier this year). And now the Russian steep discount is gone, taking longer than one would expect, and further tightening the market, a somewhat common trend when certain Asian countries (such as China and Japan, big LNG buyers) go into the market and secure their supplies.

Leading us to the inevitable scenario in which in the face of the energy crunch, high costs, inflation, and outpriced of cheap fuel, countries rich and poor alike would shift towards coal. A monumental backfire of the policies of the green elites, which I often tweeted about it, is how many of these people's policies often cause the problems they supposedly attempted to fix. India being one of the biggest producers and consumers in the world is also following China’s footsteps and shifting hard to coal, openly stating it won’t transition any time soon.

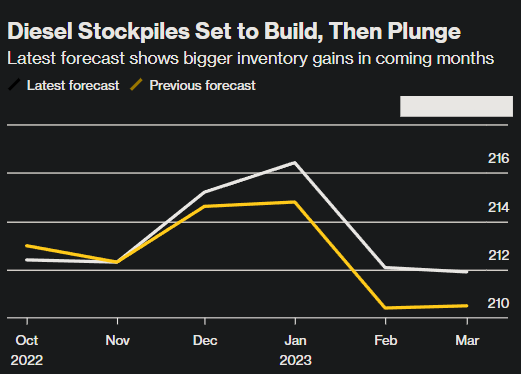

For last in the fuel section, a shortage that I have written and warned about for months, diesel, the world runs on diesel, and shortages of it have outsized impacts in every single aspect of modern life, especially growing and transporting food (and other goods, but food is arguably the most important aspect of this).

Worst of Europe’s Diesel Crunch Will Hit in Spring

Wood Mackenzie sees diesel inventories at record low in March

EU to cut off seaborne deliveries of Russian fuel in February

With the European Union set to cut off seaborne deliveries of Russian fuel in early February, the continent’s already tight supply situation is at risk of worsening. Stockpiles are a vital cushion against such disruptions, and when they run low, there’s more potential for market volatility.

A similar trend is occurring in the US, but for different reasons, end results are similar, short-term the diesel shortage will bite the global economy, it will hinder both growth and recovery, and it might end up affecting farming, among other industries. As LNG, this also has no short-term fix, given the refining capacity lies elsewhere and with tougher Russian sanctions at play, the refining of Russian oil will shift to other countries and medium-term this will give rise to problems since it can very well fuel the funding of Western adversaries. The IAE (International Energy Agency) sounded the alarm about diesel earlier this week.

Diesel may be the next pain point in Europe’s energy crisis, with EU sanctions on Russian exports set to increase competition in an already “exceptionally tight” market, the International Energy Agency has warned.

Once an EU embargo on imports of diesel and other refined products from Russia is implemented in February, the market will tighten further, it added.

“The competition for non-Russian diesel barrels will be fierce, with EU countries having to bid cargoes from the US, Middle East and India away from their traditional buyers,” it said. “Increased refinery capacity will eventually help ease diesel tensions. However, until then, if prices go too high, further demand destruction may be inevitable for the market imbalances to clear.”

Global supply problems have been exacerbated in recent months by industrial action at European refineries. Walkouts over pay at several refineries in France led to fuel shortages across northern France in October and at one point helped to propel diesel prices in the main European trading hub of Rotterdam to more than $80 higher than the price of crude oil, the IEA said.

This leads us to the conclusion of this section. In summary, given the ongoing trends and the probabilities of other events taking place or the further impact of current trends, you now have enough data and observational evidence to safely trace a roadmap for what 2023 will look like if nothing else goes wrong. And 2023 is shaping up to be a horrible year from all angles, one in which the virus and all it entails get out of the spotlight, new narratives to hide the vaccine damage and propaganda war will be produced and set upon the world, and the costs of 2020 finally catching up to us.

The war in Ukraine accelerated the degradation of the current system, fuel, and energy shortages, be they for a fleeting moment or for days in the end will occur globally, richer regions might be able to tackle such changes at a better pace than poorer regions, but this will definitely impact the whole supply chain, poorer countries are the de facto producers of many goods the world needs.

The very first Beyond Mathematical Odds was about how hybrid warfare was potentially playing out, and this is my preferred angle to do analysis. Months back Freeport LNG, one of the major hubs of export of liquified gas to overseas customers suffered an “accident”, an explosion/fire, and the port administration told it would take some time to get back, after a few delays the new deadline is mid-December. El Segundo, Chevron’s oil refinery recently suffered a massive fire too. A recurring problem within the Lawas pipeline in Malaysia had a fire incident, further affecting the Asian gas market. And earlier today a massive explosion in a gas pipeline near St. Petersburg, Russia.

These are a few incidents, but why do I bring them up here ? Because as previously noted, “accidents” and weird events will take place with more frequency, both from a cascade failure perspective (running everything on maximum output for too long, without proper maintenance and for disruptive (hybrid war) reasons.

If 2023 will be marked by anything, it might as well be by unforeseen events changing global dynamics and the widespread implementation of hybrid warfare by all types of actors, state or non-state, private, and public.

I will end this piece here, and Part II will come shortly most focused on food/grains. I want you to remember what I wrote months ago.

Revolt is the most contagious human state, and one of the most contagious “memes”

When countries get desperate, be it by energy shortage, food scarcity or the influx of untold amounts of migrants, it will be “every man for himself”, they will resort to resource nationalism, as it occurred multiple times this year and last year, at many different levels and much-needed materials for the function of the global economy and production goods.

This article ends here, I intend to go back and write these more frequently, but I find myself undecided on how frequently I should write them. Not the biggest fan of very short, lacking substance writing. I also plan to write things outside everything I wrote so far.

I welcome and appreciate the support of those who choose a paid subscription, or who decide to buy me a coffee whenever they feel like it, and everyone who shares my Substack. Without all of you, this wouldn’t be possible.

Your thinking is always deeply enjoyable and overwhemingly relevant on multiple levels of existance, thriving or struggling. Thank you for writing about Energy. I love this article so deeply that I am speechless. It confirms all of my investment thesis, which makes me deeply deeply happy. Life changing happy. The incoming energy crisis will offer opportunities like nothing else has in my life time. Of course the risk of dying from bioweapons or being killed in some sort of social upheaval kind of event remains huge. But surviving that and investing the right way omg what an adventure! A lot of money could be made in the years ahead of us. Thank you for writing about energy.

PS What breaks my heart is that some people, people who live from state pensions, who worked hard all their lives and put all their savings into the bank account might be faced with hard times. That is what motivates me to invest in Markets. The thought of being able to help some people, people that I never met, that I find living at the edge of poverty somewhere ...far away, away from Twitter, hedge funds etc...the thought that I can just knock on their door and do something life changing for them is what gives me joy and make hours sitting infront of my charts worth while.

"Germany is under severe and real threat of deindustrialization"

That's not a threat, but rather a promise! By the green party. Not only for 2 years. Only their voters don't seem to get it, or agree it needs to be.

Green R.Habeck, minister of economics (of all things) now seems to be hauling in a Blackrock broad, Elga Bartsch, who is supposed to "analyze economic risks of _climate change_" (and not maybe the recipes supposedly against it?...)