I don’t recall ever putting a warning in my pieces, but if you get emotionally affected or distressed by some of these, you should avoid reading this one.

This will be a many-fold write-up, I will often refer back to things I wrote earlier this year, as usual many of the dynamics I observed and forecasted came to pass, and lately to a worsening degree than the original observation, and some to the same level I described. Cascading failure has that effect on systems. And as a friend recently wrote, we came full circle in regards to SARS-CoV-2, with many papers now being published proving many of our observations and research.

And in many regards, almost a year after, we are coming full circle on this subject. The tweet/Substack piece below serves as a point of reference, and to keep it a little more structured, I will go in parts. Food/grains, energy, and lastly what the energy state entails, and these 3 create a negative feedback loop.

Per what I wrote specifically in the piece above, my slightly broad forecast on weather shifts, regardless of the actual cause, came to pass. From too much rain to unprecedented drought in some ways, and sometimes localized, sometimes nationwide. Both are incredibly disruptive and destructive to people, farmland, and industry.

Drought has been affecting everything, from logistics of using boats to transport goods and fuel, to energy but for now, we will discuss farming, by far the most impactful aspect of it all.

For months I covered the weather conditions, paying special attention to drought conditions in what is called the US crop belt, concerned not only about the fertilizer situation, which many downplayed correct or not about it, but the weather. And so we have this.

In the east, though, things aren’t so bad. Plentiful rains have helped keep soils moist in parts of Indiana and Ohio. The outlook for yields varies by farm, even by acre. But in some places, there’s optimism that conditions are good enough to beat historical averages.

Nebraska Corn Is ‘Done’

He’s seen fields so dry that corn plants aren’t even producing ears of grain.

“I’ve been on crop tours for 16 years, and I’ve never walked into a field that had no ears,” Meyer said. “Is there anything in the east that can make up for what we saw in Nebraska over the last two days?”

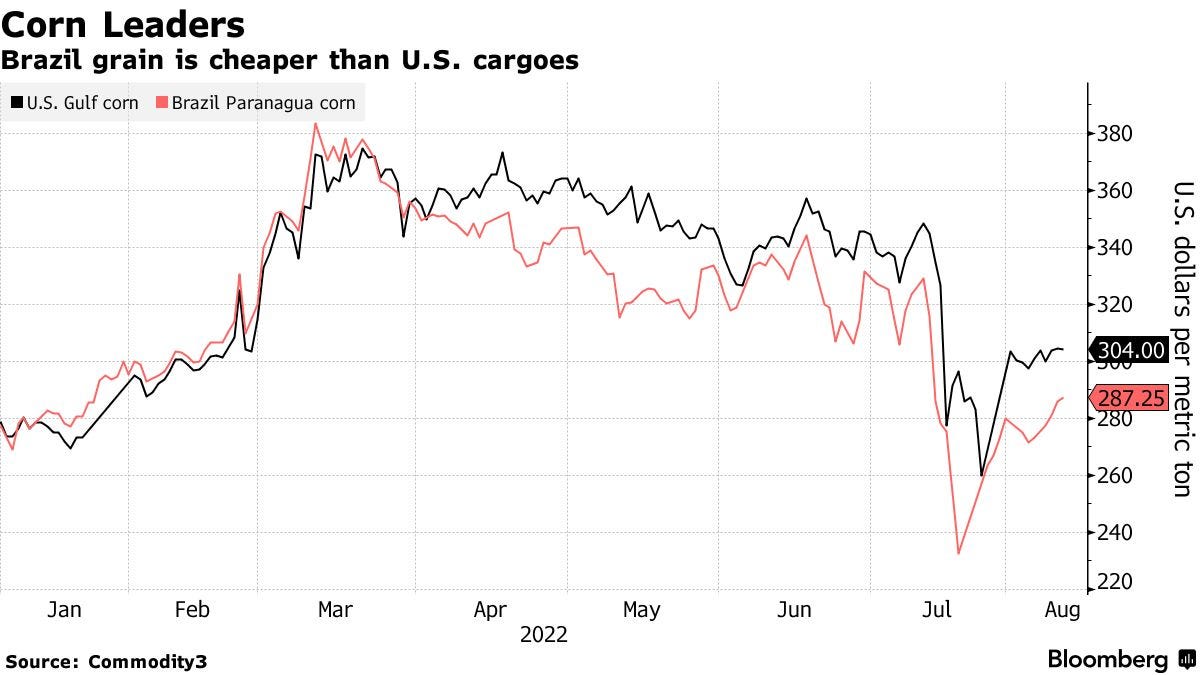

Iowa is the US biggest corn producer, and as previously written these drastic changes are sometimes localized, huge swaths of the corn-producing land were hit by excessive heat and dryness, and a lot of these fields were falling below historical averages.

Any meaningful hit in the production of North American corn will impact domestic and international prices. Corn is used as animal feed, to produce other food additives and as biofuel, any meaningful hit means Brazil has to pick up the slack. And now the US is bound to harvest the smallest crop since 2019, this will inevitably negatively impact domestic food prices, and there are other reasons for this negative impact too.

The drought conditions in parts of the US is so severe that California has now 530.000 acres of farmland without use, and California is a major producer, and guess which crops are the most affected in the state ? Rice, and Cotton. The decline in production is to be expected, which in turn will push the inflationary pressures upwards by itself.

Thankfully despite all the problems this entire year brought, and given the fast thinking (but heavily criticized by the media around the world) of Bolsonaro, getting deals for Russian fertilizer while most of the world went without, Brazil is set up to harvest almost record yields of its second corn crop. Leading China to expedite imports.

Beijing will temporarily waive a key clause which paves the way for Brazil, the biggest exporter behind the US, to ship corn to China in the coming months, according to people familiar with the matter. This follows a deal in May that guarantees Brazil access to the world’s top grains market over the long term.

That agreement, which took years to conclude due to phytosanitary concerns, requires the Brazilian government to provide guidance to farmers on chemical application and crop management prior to seeding to ensure growers take measures to avoid diseases. China will waive this condition for the current season, said the people, some of whom asked not to be identified because they’re not authorized to speak publicly. If the rule still applied, it would hinder shipments as it was imposed after the start of planting

As I wrote since the very inception of this Substack, countries will walk back any and all policies and measures that were put in place for geopolitical and economical reasons before, if that gets in the way of stability and food security. Of course, by countries, I meant non-suicidal ones, which automatically excludes the US, Canada, and the entire European continent.

As since I mentioned Brazil. As I wrote earlier this year, Brazil came to be one of the most important food producers on the planet, with the industry itself running to find solutions over the past couple of months to deal with the fertilizer situation in the country.

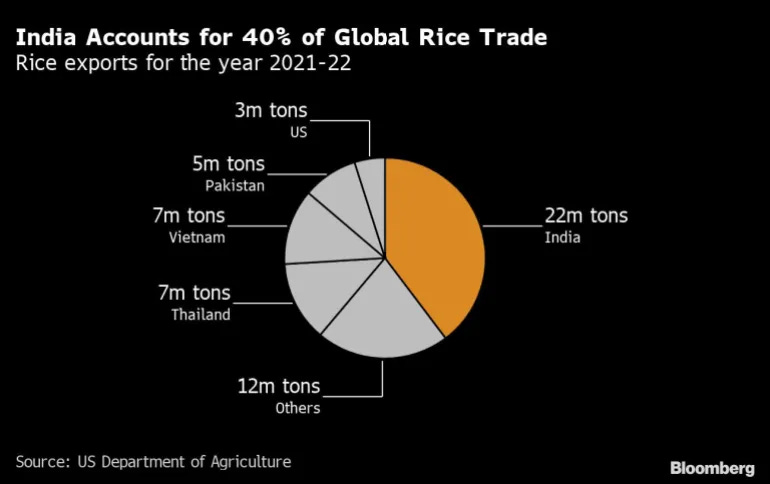

But corn isn’t the sole staple in the world. For quite some time now I have been warning of an alarming trend, imperceptible when observed linearly, deeply concerned from a complexity, non-linear approach. The staple consumed by most of the global population. Rice.

A shortage of rain in parts of India has caused the rice planting area to shrink [File: Anindito Mukherjee/Bloomberg]

Rice could emerge as the next challenge for global food supply as a shortage of rain in parts of India, by far the world’s biggest exporter, has caused planting area to shrink to the smallest in about three years.

The threat to India’s rice production comes at a time when countries are grappling with soaring food costs and rampant inflation. Total rice planted area has declined 13% so far this season due to a lack of rainfall in some areas, including West Bengal and Uttar Pradesh, which account for a quarter of India’s output.

Much is riding on the rice crop in India and the monsoon’s progress. Some agricultural scientists are optimistic that there’s still time to continue planting and make up for some of the shortfall. Rain is forecast to be normal for August to September, which may improve crop output.

Farmers are less upbeat. Rajesh Kumar Singh, 54, a grower in Uttar Pradesh, said he planted rice on only half of his seven acres (2.8 hectares) of land due to a lack of rain in June and July. “The situation is really precarious,” he said.

India seeks to boost ethanol production using surplus sugar and rice as part of efforts to cut its fuel costs. Surging food prices following the war in Ukraine have increased the risk of hunger and sparked a “food versus fuel” debate.

“At this point of time, it is difficult to estimate the exact level of production loss,” Hussain said.

As I said in Chaos Engineering any substantial effects on rice production, especially in India, will have substantial impact on global prices, food avaliabily, and as a cascade effect the possibility of social unrest. Also similar to other countries India finds itself between a rock and a hard place.

Without cheaper fuel, prices of everything are pressured upwards and using food to produce fuel drives the price of staples up internally, leading to curb exports, and that alone cascade into the immutable laws of physics, but applied to geopolitics. Every action gets you a reaction. India is a massive country, a big producer of a myriad of things and any disruptive effect on its agriculture or industry has a global effect. And countries in the region are already facing the situation, Nepal is going into a rice shortage, Sri Lanka's rice crops are failing. A key official from the Philippines already warned the country will suffer a rice shortage in the coming months, because of the drought in China.

Another trend that plays in almost every other commodity, be it food or metal or energy is transportation. Logistics are often the bottleneck in local shortages, as in some regions in India. I will cover this later in regard to coal.

A shortage of rice, or merely skyrocketing prices will inevitably lead to the potential collapse of poorer countries. And guess who is one of the biggest rice importers from India ?

The hardest hit provinces are in southern and central China, especially along the Yangtze River, and officials have called for water conservation by agricultural, commercial, and industrial users. By contrast, provinces in China’s northeast have experienced beneficial weather for much of the growing season.

In several of China’s southern rice producing provinces — Jiangsu, Sichuan, Anhui, Jiangxi, and Hunan, which together account for nearly half of total rice production — Gro’s vegetative health index, a satellite-derived measure of plant health, is at the lowest level in more than two decades. In addition, soil moisture levels are at a 12-year low, and Gro’s Drought Index reading is elevated. Those adverse conditions come as China’s rice crop is in its critical grain filling stage.

Although China is the world’s largest wheat producer, the country is also a sizable importer as demand, including for animal feed, outpaces domestic supply. Wheat imports in 2021 and so far in 2022 have far outpaced historical averages, Gro data shows. For 2022/23, China is forecast to import 9.5 million tonnes of wheat and 6 million tonnes of rice, according to the latest USDA projections.

Drought also is hitting China’s cotton crop ← important later on

As I wrote in Food Scarcity and Water Wars one of the biggest worries of many countries in the very near future is water availability, and this is one of the main drivers of Chinese aggression toward its close neighbors. Covertly it is what drives countries in the Eurasian region into some forms of dispute and the same applies in the Middle East recently.

China's water crisis hits are many-fold as per usual, not only hitting the food production of a massive importer (a reminder that in 2021 China bought 51% of the total global production of grains), and also affecting energy generation, hitting many of its hydroelectric stations. As I wrote on Twitter quite a few times this week, we will experience similar events but the result will be from different dynamics, or perhaps if one is inclined to observe from a complex system perspective, these are the results of decisions made between June and October of last year and we are merely living on its cascade effects.

China can still outbid almost all other countries on the planet for any resource it needs, and fuel is one of them, the massive loss of crops and yield in China will certainly reflect on its importing habits and will once again drive food inflation upwards.

And since drought definitely affected the energy market.

Energy, fuel, and the loop

The biggest problem with China reverting to coal, at least from my perspective, isn’t green beliefs, but market dynamics. The continuous stupidity by the EU elites, its vassal states (governments of each nation), the ineptitude of the US government, and a few accidents here and there, and the noxious fact the world relied much more on Russian commodities than most are willing to accept lead to both coal and gas beating record prices, and energy costs are now, on a daily bases, beating historical European prices.

Russia, not only a major gas but also a major coal exporter is willing to sell. Shortsighted emotional “leaders” unwilling to see or unable to understand and insisting on self-destructing decisions are harming their own economies and industry on both local and global scales. Poland now has a coal shortage. Poland. One of the biggest coal exporters in the EU.

And the easiest way to appease the population is by subsidizing, which will once again push energy prices upwards, won’t solve the supply problem, and inevitably lead to further dysfunction. And similar to China, burning any quality of coal for the sake of keeping its industry and household supply “steady”, Poland and in fact, many other countries will burn dirty coal. Ironic, that in the pursuit of the green dream, they will end up polluting the planet even more.

Germany is already worried it won’t have enough coal and oil for the Winter, and at this point, it is not an if, it is “how much”. At least some parts of the German ruling class are sensible enough to revert some decisions that will deeply impact the country.

The agricultural ministers of the German states have officially approved a proposal by federal minister Cem Özdemir to allow the cultivation of productive crops on certain fallow land in light of the war in Ukraine.

According to the decision taken on Tuesday (16 August), farmers may continue to grow cereals, sunflowers or certain legumes for one year on land that they would otherwise have been obliged to take out of production under the reformed EU Common Agricultural Policy (CAP), which will start being applied by EU member states from January 2023.

Contrary to Özdemir’s original position, Germany is thus partially implementing the derogation proposed by the EU Commission at the end of July, which allows member states to relax certain environmental requirements within the CAP in light of the impact of the Ukraine war on global grain markets.

The reason I am sharing this one is not much for the “good news” aspect, but to once again demonstrate that all poor decisions, all cascade effects and almost everything going wrong in Europe is a result of the EU. Like banning Russian coal, a decision that went into effect some days ago.

UK households are now expected to experience a £6,000 per year as soon as April next year. Dozens of millions are expected to go into energy poverty in the United Kingdom alone, with millions of homes freezing attempting to save some money to quite literally survive and buy food.

A light on in a residential house at dawn in the Stalybridge district of Greater Manchester. Photographer: Anthony Devlin/Bloomberg

Energy firms in the UK are also refusing to supply small businesses because they don’t expect said businesses to be able to tackle the increasing energy costs. While a different trend plays elsewhere in the continent, the drastic effects are similar.

The aluminum output (production) loss in Europe alone has already lost 1.000.000 tonnes and right now between the US and Europe they can add another 750.000, and the expectation is that Asia can pick up the “slack”. Which creates the first loop and a conundrum.

Aluminum is used in almost every single aspect of both industrialized society, and our daily lives but especially in green technology, and as I wrote months ago, any hiccup in the aluminum output would severely impact the transition to green energy. Solar panels use a lot of it, and so does electronics manufacturing, among many other important uses. A significant loss of production will have yet another impact, as it did twice in the last 18 months. Another shortage that has been building up, and intensifying is copper.

I would also want to note that the US is also experiencing severe difficulty in tackling energy prices with as many as 20 million households behind their energy bills, and the rest of the planet is either in a worst state or soon to follow.

But if those were the only problems with high energy costs, one could say “things will be fine shortly”. But energy prices deeply impact fertilizer production.

Fertilizer shares are gaining after Azoty, Poland's biggest chemicals company and the second largest producer of mineral fertilizers in the European Union, said on Tuesday it stopped production of nitrogen fertilizers and cut output of ammonia because of record gas prices, according to Bloomberg.

Yara International (OTCPK:YARIY), Azoty's larger European peer, curbed production last month, and Anwil, a petrochemical unit of Poland's biggest refiner PKN Orlen, also stopped fertilizer production this week, citing unfavorable prices.

Different dynamics, same cause (governmental stupidity), weather shift, similar end results. We have been experiencing, almost continuously a drop in fertilizer manufacturing, especially in Europe, and if you want to be aware of how further the drop is, it is over 50% and I wouldn’t be surprised if by December the drop in fertilizer production reaches 70%.

And here we find another part of the loop. Weather shift and governmental ineptitude cause a big loss of yield on crops, which further leads to less fuel and energy, leading to less fertilizer production, among other products from commodities. Which leads to further loss of energy.

Most of my observations and tracking down and data gathering on these issues were born from the first lockdown, nature is one of the most complex systems we know, but also the most adaptable, the planet will often “correct” itself, so it didn’t take long for me to observe, research and forecast where that decision could shift. Yes, from the single decision of locking down the entire planet, with some adjustments, I was able to forecast the dynamics far into 2021 and early 2022.

Why I am sharing this ? Because the same dynamic played last year with parts of the world halting industry activity, not as drastic as 2020, but enough that I thought it would fuel the shift, is being played again, at a larger scale by what we covered in the Energy section. Here is a great piece on how energy costs affect food and farming.

I could elongate this piece almost ad infinitum, adding many of the other aspects affecting what I am about to write (if there is interest just say and I will do so), but for now, I will end it here.

What the West, and possibly the entire planet is about to experience, is the slow (for now) breakdown of a complex system, things are breaking down faster than we can replace them, or even produce them. Countries are increasingly more resource-aware and nationalistic about it, India earlier this year went from “we will export wheat to the entire planet”, to “we might ban the export of wheat”, and is now contemplating banning the export of wheat flour to tackle prices. Norway is weighing the possibility to halt energy exports leading to its neighbors and the EU getting “big mad”.

As Kairon from Mercurial Space said a few days ago, doesn’t feel like many people played Diplomacy (the board game). For most of the existence of our civilization on its many interactions, alliances were never about anything but resources. And our brief period was an outlier one, and this shall be the norm again.

I will once again repeat two things. No government will collapse itself, unless pressured by outer influences. And please stock some damn food. As I forecasted earlier this year and being completely ignored by all but one person, there will be a substantial global loss of yield, the Everything Shortage is once again back, and it is stronger than before.

To get a broader picture I strongly recommend you to read my other Beyond Mathematical Odds, if anything to see if my track record is accurate, or how things played out in the long run.

I thank all the supporters here and on Kofi and appreciate all of you ! I often end these longer pieces with a Kofi link and a message. I will end only with a single message this time.

You can support my work anytime you wish but today, I won’t ask you to become a paying subscriber, I will ask you this. GO BUY AND STOCK SOME DAMN FOOD. You can become a free subscribers, and sharing articles you find useful is very helpful.

In this context it is emotionally rending to be right. There are so many complex threads merging right now including massive intentional harm having been applied to increase disruption among we, the population, with a cascading effect. And with the addition of climatic trends we simply fail to understand at a popular level. Hard to do right when everything surrounding is bent on doing wrong.

Excellent as always. You are very insightful and logical and you connect the dots well. So many people don't hear my warnings. I feel like Cassandra.

In this context it is emotionally rending to be right. There are so many complex threads merging right now including massive intentional harm having been applied to increase disruption among we, the population, with a cascading effect. And with the addition of climatic trends we simply fail to understand at a popular level. Hard to do right when everything surrounding is bent on doing wrong.